Guide to Buy a Home in New York 1.2

Thinking about purchasing a home?

1.2

Downpayment

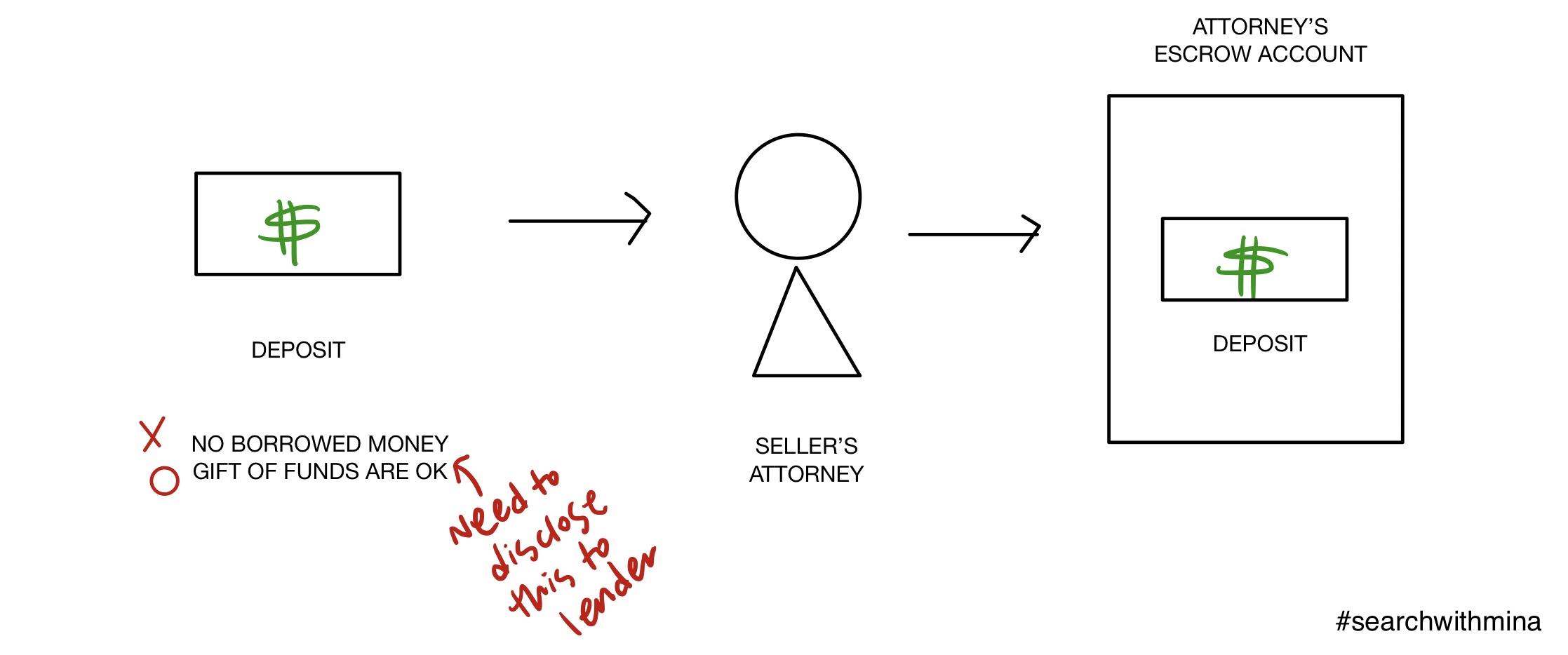

When you sign a contract to purchase a home, you will be required to simultaneously make a downpayment equal to ten (10%) percent of the purchase price (usually for coops), although when purchasing new construction you may required to make an additional downpayment of up to fifteen (15%) percent of the purchase price. The downpayment may be made by personal check, and it will be made payable to the seller’s attorney who will hold the money in an attorney escrow account until the closing.

In general, when obtaining a loan to buy a home, any funds that will be used for the downpayment and any other funds that are used to pay for the home (other than your bank loan) must come from your own savings. No money can be borrowed from any source, i.e., no credit cards, no personal loans, and no credit lines can be accessed. However, you may be able to receive a gift of funds for the downpayment or a portion of the purchase price as long as you disclose this to your lender in your loan application and provide a gift letter (to indicate that you do not have to repay the money given to you).

Closing Costs

As you begin to determine how much money you will need to purchase a home, you must also consider the costs associated property you are purchasing and the type of loan that you select. Generally, closing costs for a house or condominium apartment (i.e., real property) will be greater than those for a co-operative apartment (i.e., personal property). When purchasing real property, you must purchase title insurance and pya a mortgage recording tax on your loan amount, whereas title insurance is not necessary when purchasing personal property and as of the date of 7/18/2018, there is no mortgage recording tax on co-op loans. Purchasing a co-op apartment or a condominium unit from a sponsor or developer will also increase your closing costs substantially as you will see in later blog.

Monthly Expenses

Besides your monthly loan payment, there are other costs of owning a house, co-op, or condo apartment. In a co-op, these charges are called “maintenance” and in a condo, they are called “common charges”. These monthly fees cover a share of the cost of operating the building, such as the utilities for the common areas of the building, salaries for building employees, real estate taxes, and property insurance. These operating expenses are apportioned to each co-op or condo unit owner based upon the approximate proportion that the floor area of a unit relates to the total square footage of all units in the building, the location of the apartment within the building, and number of rooms in the apartment. In the case of a co-op, the monthly maintenance payments include real estate taxes and homeowner’s insurance are not included in common charges and should be factored into the calculation of monthly expenses. Taken all together, the monthly costs of owning a home are typically referred to as “carrying charges”

Qualifying for Financing:

Pre-Qualification vs. Pre-Approval vs. the Loan Commitment

The quickest way to determine how much you will be able to borrow for your home purchases is to pre-qualify for a loan. In order to obtain a pre-qualification, you simply contact a lender by phone and provide your income, assets and liabilities to the loan officer. After evaluating this information, the loan officer will advise you of the loan amount for which you would qualify. Loan pre-qualification does not include a credit check, a verification of the information that you have provided, or a review of the home that you are interested in purchasing, so it is NOT a sure thing. The pre-qualified loan amount will, however, give you a good idea of how much you will be able to borrow.

Pre-approval is the next step in the financing process. To obtain pre-approval, you will need to complete a loan application and provide the loan officer with the necessary documentation for the lender to verify your income and assets, including copies of your tax returns for the previous two years, pay stubs, W-2 statements and your most recent bank statements. The loan officer will calculate your debt to income ratio, examine your outstanding debts and other monthly financial obligations and order a credit report to examine your credit and payment history with credit cards and other loans. After this process is completed, you will receive a pre-approval letter for the specific mortgage amount for which you are approved.

Obtaining pre-approval letter gives you an advantage in a competitive bidding situation, as the seller will know that your are qualified for financing and are one step closer to obtaining a loan commitment.

Once you have signed a purchase contract and submitted it to your lender, the final step in the loan qualification process is obtaining a loan commitment. A loan commitment is a formal pledge by the lender to provide you with a loan of a specific amount, subject to the property appraising at or above the sales price and final verification of your income and assets confirming that your credit profile has not changed since you submitted your loan.

Source: Keith A. Schuman, Esq